Functionality of the blockchain

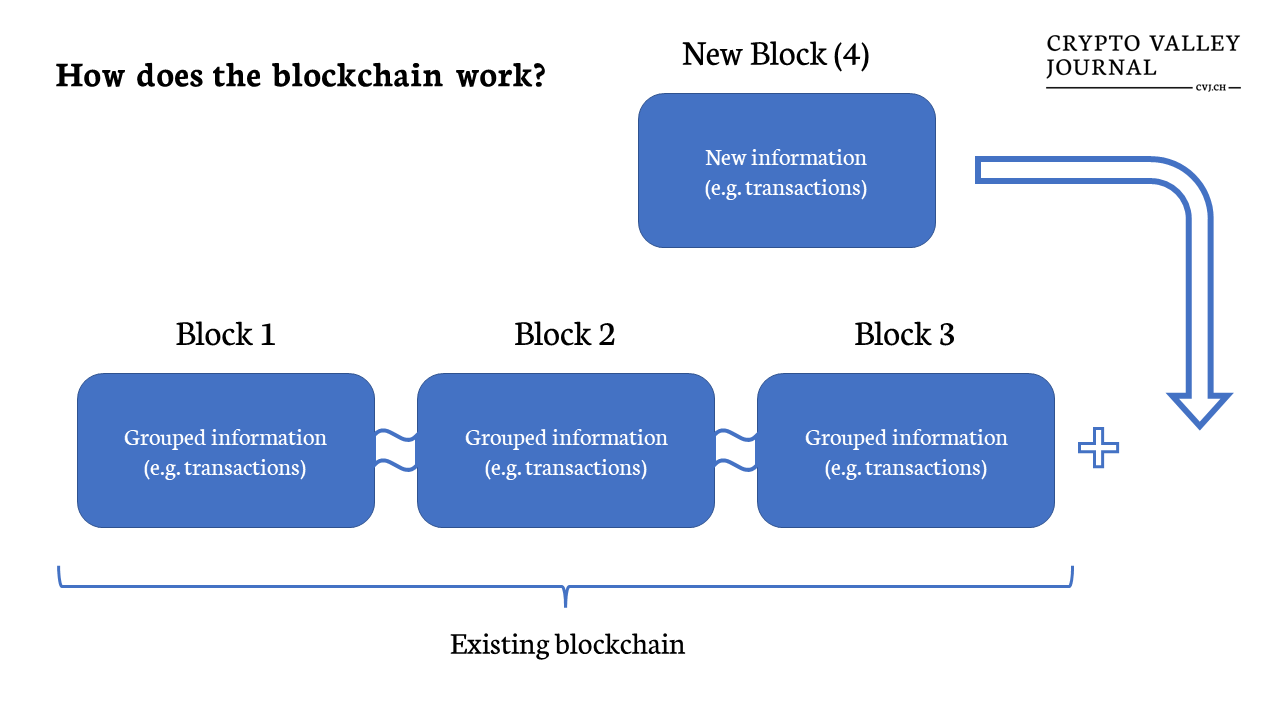

One significant difference between a typical database and a blockchain is the way data is structured. A blockchain gathers information into groups, also known as blocks, which contain transaction information. Blocks have specific storage capacities and, when filled, are attached to the previously filled block. This creates a chain of data known as a “blockchain.”

A database structures its data in tables, while a blockchain – as the name suggests – structures its data into groups (blocks) that are linked together. Thus, all blockchains are databases, but not all databases are blockchains. This decentralized system generates an irreversible data history. Once a block is filled, it is set in stone and becomes part of this immutable timeline. Each block in the chain is precisely timestamped when it is added to the chain.

Decentralized structure

One of the main advantages of blockchain technology is decentralization. Conventional databases are centralized, meaning they are controlled by a single entity, such as a bank or government. Decentralized databases, on the other hand, are distributed across a network of computers, and no single entity has control over the database. This makes the database more secure and less susceptible to hacker attacks or privacy breaches.

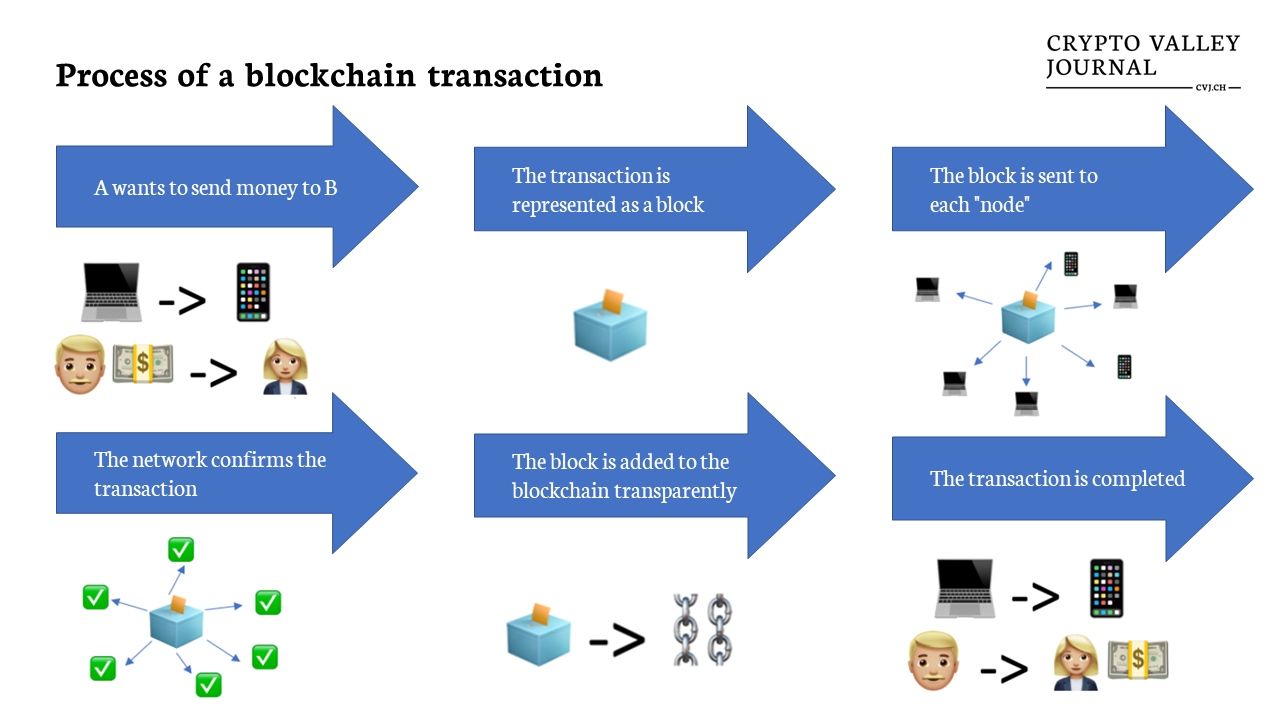

New information added to the blockchain in the form of blocks is constantly synchronized with the database, which is stored in multiple locations and updated periodically. All records in this database are public and verifiable. Since there is no central location, manipulating the system is difficult, as the information exists simultaneously in multiple places.

“Imagine a spreadsheet that is duplicated thousands of times across a network of computers. Then imagine that this network is designed to regularly update the spreadsheet. That’s a basic understanding of blockchain technology.” – Ameer Rosic, Blockgeeks

Unlike a traditional computer, a blockchain network can offer strong guarantees of trust based on the cryptographic and game-theoretical properties of the system. For example, a user or developer can trust that code executed on a blockchain computer will continue to behave as planned, even if individual computers in the network attempt to undermine the system. This allows a blockchain network to facilitate disintermediated, peer-to-peer interactions and digital services owned by communities rather than corporations.

Blockchain technology uses cryptographic algorithms to ensure the security and integrity of data. Each block in the blockchain contains a unique cryptographic hash, which is generated based on the data in the block. This hash links the block to the previous block in the blockchain, creating a chain of interconnected blocks. This process of linking blocks creates a permanent and immutable record of transactions.

Challenges of blockchain technology

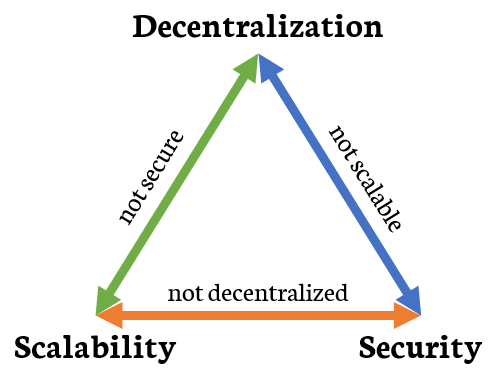

Scalability: One of the biggest challenges of blockchain technology is its scalability. As the blockchain grows larger, more time and resources are required to process transactions. This can make the use of the blockchain slow and expensive, especially for applications that require a high volume of transactions.

Interoperability: Another challenge of blockchain technology is interoperability. There are many different blockchain platforms and protocols, and they are not always compatible with each other. This can make the transfer of data and value between different blockchains more difficult.

Regulation and Acceptance: Blockchain technology is still in its infancy, and there are many challenges in terms of regulation and adoption that need to be overcome. Governments and regulatory bodies are still grappling with how to regulate blockchain technology, and many companies and organizations are hesitant to adopt it due to concerns about security, scalability, and interoperability.

Use cases of blockchain

Blockchain is already being used in many areas. It can be distinguished between closed and open systems. While cryptocurrencies mostly operate on open systems, many companies have internal blockchain systems in operation that they maintain themselves. As blockchain technology matures and evolves, it is highly likely to be increasingly used and integrated in various industries and applications.

The use cases are extensive and mainly occur in areas where the properties of tamper-proof transparency are required. This requirement can be important in logistics, supply chains, administration, and, of course, the financial sector. Proposed as a research project in 1991, the concept of “blockchain” has now reached its late twenties. Over the past two decades, it has increasingly captured a significant portion of public attention. Companies around the world are elaborating on what the technology is capable of and how it will evolve in the coming years.

With many practical applications, blockchain technology is attracting global attention, not least due to Bitcoin and other cryptocurrencies. A buzzword on the tip of every investor’s tongue, blockchain is about making business and government operations more precise, efficient, secure, and cost-effective by reducing intermediaries. As we prepare for the third decade of blockchain, it’s no longer a question of “if” but “when” established companies will embrace the technology. The functions that blockchain can already assume in our daily lives are evident in our coverage of the topic.

Summary