The two most popular Bitcoin valuation models are PlanB's Stock to Flow model and Willy Woo's NVT ratio. The SwissRex model combines these two models and includes monetary and fiscal policy.

Stock to Flow

The Stock to Flow ratio was first described in 1997 by the Hungarian professor Fekete. [1] The Stock to Flow ratio relates the inventory of a precious metal to its annual production. The higher the Stock to Flow ratio, the less the impact of a supply shock on the price of that precious metal.

Gold first established itself as a store of value because it was rare. However, gold owes its triumphal march over other rare precious metals to its high Stock to Flow ratio, which has led to higher price stability compared to silver, platinum or palladium. Saifedean Ammous recorded this in the book “The Bitcoin Standard” and explained that Bitcoin should prevail as digital gold.

Stock to Flow Modell of "PlanB"

Under the pseudonym PlanB, a quantitative Stock to Flow Model was published for the first time in March 2019, which states that the Bitcoin value depends solely on the Stock to Flow ratio:

PlanB Stock to Flow Modell:

Bitcoin valuation = f (Stock to Flow)

Every four years the number of newly created Bitcoins or the flow is halved, which leads to a higher Bitcoin valuation according to the Stock to Flow model. Since this has been invariably programmed into the software, it is a deterministic model, as known from natural sciences or mechanics. Monetary and fiscal policies have no influence.

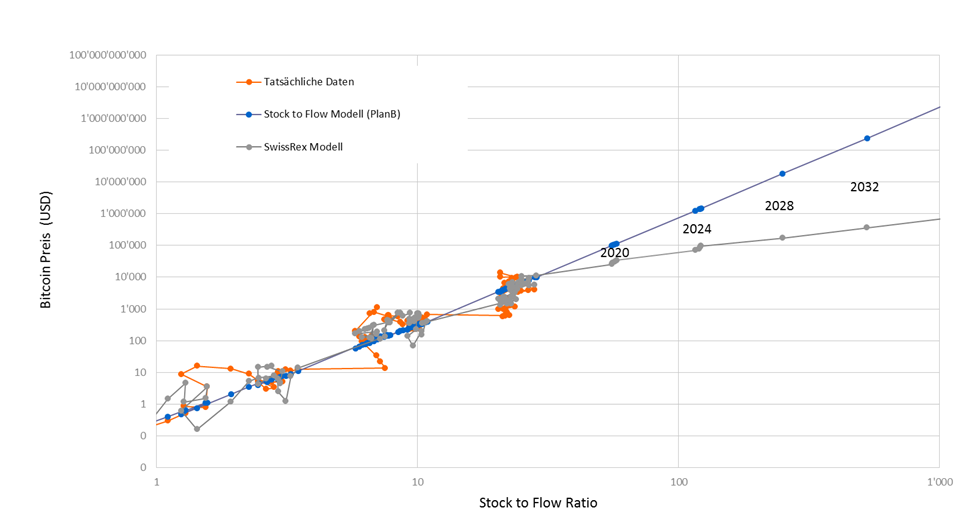

The blue dots in the graphic below correspond to PlanB's linear Stock to Flow model. Extremely high Bitcoin prices are forecast for the next few years. The price should fluctuate around USD 100,000 in 2020 and USD 1.3 million in 2024. In response to criticism, PlanB defended his model arguing that negative interest rates and money printing would enable these high price targets. However, as mentioned earlier, monetary policy or the global money supply aren’t modeled at all.

SwissRex Model

Another inconsistency appears when considering lost Bitcoins. After all, estimates assume that lost Bitcoins could be up to 20% of the Bitcoins in circulation. With PlanB’s model, this can only be factored in by reducing the amount of Bitcoins in circulation. However, this reduces the Stock to Flow ratio and lowers the Bitcoin value according to the model. Logically, the opposite would be expected: lower supply leads to higher Bitcoin prices.

SwissRex Modell

Above, reference was made to the incorrect specification of the PlanB Stock to Flow model. The SwissRex model eliminates these shortcomings. The derivation is based solely on the assumption that the supply and demand for goods, services and securities must match. [2] The result is:

Bitcoin Valuation

= f (Adoption rate, money supply, NVT Ratio)

= f (Adoption rate, money supply, Bitcoin velocity)Adoption rate = Bitcoin transactions/global transactions = f (Stock to Flow)

The Bitcoin valuation depends on three variables; the adoption rate, the global money supply (M1) and the Bitcoin velocity. The adoption rate describes what percentage of the global transaction volume is made in Bitcoin. The velocity defines how often a Bitcoin changes hands on average per year and equals the inverse value of the NVT ratio popular in the crypto world. [3] The SwissRex model can therefore be seen as an expanded synthesis of PlanB`s Stock to Flow model and Willy Woo`s NVT ratio.

The result of the regression analysis is shown in gray in the graphic above. The relationship between the Bitcoin valuation and the Stock to Flow ratio is no longer linear, but curved, which is why we also call this part of the model Capped Stock to Flow model. The cap comes from the fact that the adoption rate can be a maximum of 100%.

In the SwissRex model, the adoption rate is only determined by the Stock to Flow ratio. This is based on the assumption that a higher Stock to Flow ratio leads to a shift in the portfolio allocation in favor of Bitcoin. Other factors such as network effects have been tested, but so far no significant relationship has been found. This suggests that Bitcoin is primarily viewed as digital gold and not as currency. In the SwissRex model, lost Bitcoins lead to a lower average Bitcoin velocity and thus to a higher Bitcoin price, as is logical.

Assuming that the global money supply (M1) will increase by 10% over the next few years and the bitcoin velocity will fluctuate around the mean of 4.5, the result is a fair Bitcoin value of USD 25,000 at the end of 2020 and USD 70,000 at the end of 2024.

Conclusion

PlanB has shown an interesting approach to value Bitcoin. Accordingly, a higher Stock to Flow ratio leads to portfolio shifts towards Bitcoin. However, as we have proven economically, the specification of the PlanB Stock to Flow model is incorrect.

- The relationship between the Stock to Flow ratio and the Bitcoin valuation cannot be linear, as a maximum of 100% of the global transactions can be made in Bitcoin.

- Other macroeconomic factors such as the global money supply and the velocity must also be taken into account, which means that the model is no longer deterministic.

- The SwissRex model for the valuation of Bitcoin remedies these shortcomings and can be seen as an extended synthesis between PlanB`s Stock to Flow model and Willy Woo`s NVT ratio. A fair Bitcoin value of USD 25,000 is forecast at the end of 2020.

[1] Antala Fekete, Wither Gold? (1997)

[2] The proof can be found at https://swissrexag.ch/wp-content/uploads/1910_Newsletter-8_stock-to-flow-model-proof-of-non-linearity_EN.pdf

[3] http://charts.woobull.com/bitcoin-nvt-ratio/

[4] The capped Stock to Flow model describes in principle that part of the SwissRex model that is not determined by the global money supply and the Bitcoin circulation speed.