")

After a lot of new projects in the area of decentralized finance (DeFi) have gained traction last year, borrowing and lending have become increasingly popular topics in the crypto space. But what is the hype regarding DeFi lending models and crypto lending in general?

As we all know, lending is hardly a new phenomenon. It dates back to Mesopotamian times and even before the Code of Hammurabi established regulations, we can be sure that Peer-to-Peer (P2P) lending came in handy when you needed to borrow some barley seeds from the neighbouring farm.

What has changed, however, is the efficiency of the system. The traditional banking system improved lending through two types of centralization – centralizing capital and liquidity and centralizing risk management through a trusted intermediary. This centralization came at a cost and was not sufficiently inclusive – today many people remain underbanked.

Lending & Borrowing on the blockchain

Decentralized finance (DeFi) leverages blockchain technology and cryptography to get the best of both worlds. A trustless system removes the cost of intermediaries and improves accessibility. In addition, the complex task of managing a pool of funds (usually performed by entire Balance and Liquidity Management departments at a bank) is handled by algorithms and smart contracts.

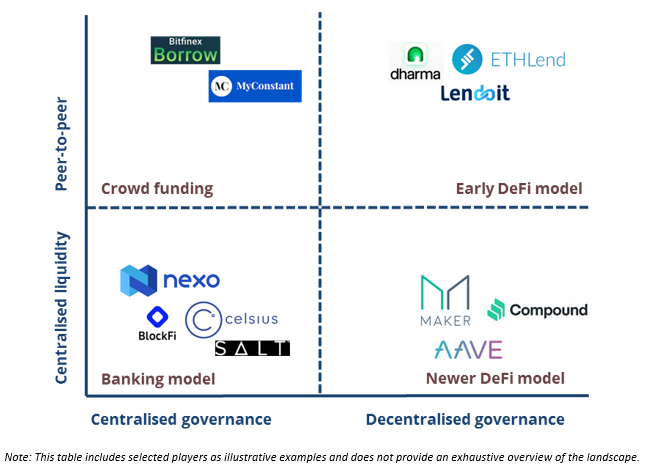

Centralized platforms with pooled liquidity

Traditionally, banks pool funds received from deposits (retail, corporate and wholesale) as well as other funding sources. Centralised platforms such as BlockFi, Celsius Network, Nexo.io and Salt perform a similar function allowing users to lend and borrow cryptocurrencies. Some of them even have their own native tokens (CEL, NEXO and SALT). Interest can be denominated in these tokens, which platforms also use to provide rewards.

These providers generally advance loans in fiat currency or stablecoins against cryptocurrency collateral (loan amount limited to say 80% of the collateral value). If the collateral value falls and the loan-to-value (LTV) crosses a threshold, they sell collateral to repay the loan. BlockFi, for example, offers USD or stablecoin loans collateralized by Bitcoin (BTC), Ether (ETH), or Litecoin (LTC). Nexo.io takes a wider selection (including PAX, EOS and TRX amongst others).

P2P funding but centralized platforms

Similar to traditional P2P lenders such as Prosper or LendingTree, centralized platforms such as Bitfinex Borrow and MyConstant offer crypto lending and borrowing.

Here, blockchain technology provides a solution to traditional P2P challenges such as transparency, enforceability, and the need to trust your counterparty. What could better solve these issues than distributed databases and self-executing smart contracts?

P2P funding with decentralized governance

Decentralized P2P lending has also been experimented with in the crypto space by ETHLend (the precursor to Aave), Lendoit and Dharma – which pivoted to a savings model. Without an intermediary, borrowers pay less, lenders earn more, and financial inclusion extends outside of the banking system.

The challenge, however, is that P2P still requires direct matching of borrowers and lenders without the benefits of centralized funding – enter DeFi lending with pooled liquidity.

DeFi platforms with pooled liquidity

The Ethereum blockchain is the foundation for many of the DeFi applications we have today. Programmable money allows decentralized lending and borrowing in terms of smart contracts. Pool-based lending protocols pool cryptocurrency deposits received from lenders in a pool contract. Borrowers access the pool of funds through the same contract, posting collateral. Required collateral is typically defined as a multiple of the loan amount (e.g. LTV of 150%).

Liquidation automatically occurs, and liquidation fees are charged, if the LTV drops below predetermined limits. Cost of funds (interest earned on deposits) and interest paid on loans are algorithmically determined based on supply and demand, as are liquidity reserves.

Implications for traditional financial institutions

Whilst crypto lending currently appears to be confined to the realm of margin trading and capitalizing on arbitrage opportunities in crypto, there are real economy applications. This poses a threat to traditional banks. However, there are also opportunities to leverage the underlying technologies to increase efficiencies in lending practises and to provide clients with access to high yield investments.

Look out for our article next week, where we take a deeper look at popular DeFi models including Compound, Aave and MakerDAO.

Copyright © 2021 | Crypto Broker AG | All rights reserved.

All intellectual property, proprietary and other rights and interests in this publication and the subject matter hereof are owned by Crypto Broker AG including, without limitation, all registered design, copyright, trademark and service mark rights.

Disclaimer

This publication provided by Crypto Broker AG, a corporate entity registered under Swiss law, is published for information purposes only. This publication shall not constitute any investment advice respectively does not constitute an offer, solicitation or recommendation to acquire or dispose of any investment or to engage in any other transaction. This publication is not intended for solicitation purposes but only for use as general information. All descriptions, examples and calculations contained in this publication are for illustrative purposes only. While reasonable care has been taken in the preparation of this publication to provide details that are accurate and not misleading at the time of publication, Crypto Broker AG (a) does not make any representations or warranties regarding the information contained herein, whether express or implied, including without limitation any implied warranty of merchantability or fitness for a particular purpose or any warranty with respect to the accuracy, correctness, quality, completeness or timeliness of such information, and (b) shall not be responsible or liable for any third party’s use of any information contained herein under any circumstances, including, without limitation, in connection with actual trading or otherwise or for any errors or omissions contained in this publication.

Risk disclosure

Investments in virtual currencies are high-risk investments with the risk of total loss of the investment and you should not invest in virtual currencies unless you understand and can bear the risks involved with such investments. No information provided in this publication shall constitute investment advice. Crypto Broker AG excludes its liability for any losses arising from the use of, or reliance on, information provided in this publication.