Blockchain networks are public infrastructure maintained by economically incentivized actors. As of today, the prevalent way to ensure security and continuous operation of major blockchains has been Proof-of-Work mining, the core innovation behind Bitcoin that first enabled the existence of stateless digital money.

In recent months and years, blockchain networks have evolved to use different incentive models to maintain their infrastructure without requiring a central authority. A clear emerging trend is the migration to Proof-of-Stake (PoS). Networks that use Proof-of-Stake rely on participants providing monetary collateral instead of expending energy, as is the case with Proof-of-Work.

Staking requires users to lock tokens in escrow and entitles them to a share of rewards the network is generating. This incentive model can be used in various contexts from deciding who participates in consensus (as e.g. in smart contract platforms like Tezos, Cosmos, Polkadot, and soon also Ethereum), to more application-specific use cases like providing blockchain data to front-end applications (The Graph), or distributing work in on-demand video transcoding (Livepeer).

The Emergence of the Staking Industry

Dating back to 2012, the concept of staking has a long history - the switch to Proof-of-Stake is a core piece of Ethereum’s roadmap and even mentioned in the 2013 whitepaper. A turning point came in 2018/19 when Tezos and Cosmos, two well-respected projects with large communities, launched and brought about an industry of staking providers - often also called validators or node operators.

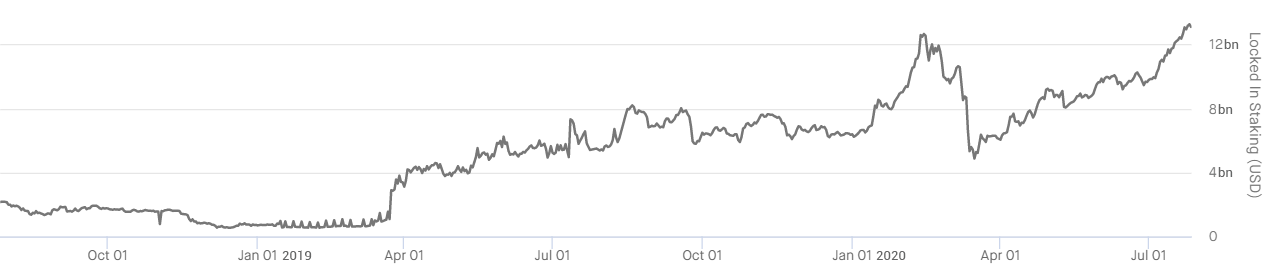

Since then, the number of networks making use of some form of staking has been continuously expanding. With a few exceptions, most newer protocols rely on some form of staking. This can also be seen when taking a look at the value of collateral locked in staking over time. At the time of writing, the value of assets that is being used for staking across different networks has grown to over $12 billion.

Total value locked in staking (in USD)

Data and graph taken from https://stakingrewards.com on Jul 27, 2020.

This trend is largely driven by new staking protocols going live and is expected to continue further due to further launches and migrations to Proof-of-Stake, as e.g. planned for Ethereum 2.0.

With $12 billion at stake and an average annualized reward rate of 12.5%, annualized earnings in decentralized networks already amount to roughly $1.5 billion a year, which has led to the formation of an entire new industry segment focused on helping token holders to participate.

The Staking Industry

Staking requires users to lock their tokens and to securely operate node infrastructure to earn network rewards. Since most token holders do not have the necessary skills or resources to do this, different options to participate in staking have emerged:

- Own Infrastructure: Token holders can operate their own nodes. This usually requires significant knowledge of network protocols and expertise in setting up secure, highly available infrastructure, making this option suitable only for a small subset of large holders and/or technology enthusiasts.

- Custodial Staking Providers: Many centralized exchanges (e.g. Binance or Kraken) and custody providers (e.g. Anchorage or Coinbase Custody) offer staking and enable users to earn rewards when storing tokens on their platforms.

- Non-Custodial Staking Providers: In most staking networks token holders are able to outsource the operation of node infrastructure to independent providers like Chorus One or Figment Networks without giving up custody. By sending a special transaction, token holders can delegate their rights in exchange for an in-protocol fee that is automatically deducted by the network.

- Node-as-a-Service Providers: Finally, services like those offered by Bison Trails and Blockdaemon enable token holders to spin up and manage their own nodes on various protocols. These white-label solutions are mostly catered to parties that are interested in offering staking to their customers under their branding (e.g. custodians, exchanges, wallets, etc.).

Which of these options makes sense is highly dependent on the stakeholder and his goals. If you are interested to learn more about this topic, I recommend checking out staking provider stakefish’s guide on how to choose a validator that provides an interesting lense on how to evaluate the various options.

Conclusion

Cryptoassets are evolving from purely speculative investments to serving productive uses. Be it staking, providing liquidity, or lending out tokens in decentralized finance; holders of cryptocurrencies need to figure out how they want to deploy their assets in the emerging decentralized economy.