"Central banks are printing lots of money." This is a phrase you hear almost all the time these days. But how exactly is new money created and where does money come from? Our monetary system has changed over time. The creation of money through credit plays a key role in this.

In order to understand the process of money creation, it is necessary to take a look at the past. From the former Gold Standard to the current FIAT system, a change has taken place. A look at the history and the process of money creation.

The Gold Standard

In the history of money, various commodities have been used as money starting with shells, pearls, silver and ending with gold. Gold and silver coins were used in parallel as means of payment, in order to make smaller units possible with the latter. Finally, these gold and silver coins were replaced with banknotes representing a claim on the gold.

The development from the direct use of gold as a means of payment to banknotes representing a claim to gold can be explained as follows: Larger quantities of gold were stored at a custodian, that confirmed acceptance by means of warehouse receipts. The warehouse receipts were then used as gold-backed paper money. Since anyone could redeem any warehouse receipt for gold at the custodian, the receipt corresponded to the actual value of the gold. The warehouse receipt is therefore not personalised and is thus referred to as a "money substitute".

In principle, custodians have the possibility to issue more warehouse receipts than they hold gold. These warehouse receipts are referred to as "unbacked warehouse receipts". In the past, this has often happened. This has far-reaching consequences: When customers of the custodian learn about the issuance of unbacked warehouse receipts, they lose confidence in the custodian. These customers then quickly redeem their warehouse receipts in order to secure their gold and thus their possession. Those who do so last will not receive any more gold, as the custodian is already empty. This is the reason for so-called "bank runs".

At the end of the 19th century, governments established the coverage of paper money by gold. Such a monetary system is called the "gold standard". It was based on the obligation to redeem banknotes, which means that banknotes must be exchanged for gold at any time at the request of the population. During the First World War, warring governments issued uncovered banknotes to finance the war. As a result, the obligation to redeem banknotes was suspended in order to prevent a bank run. This excessive printing of uncovered paper money was the cause of the subsequent inflation. Before the further history of money is told with the introduction of the next gold standard, a basic understanding of the process of issuing uncovered storage notes is first established. This requires a closer look into the process of issuing loans.

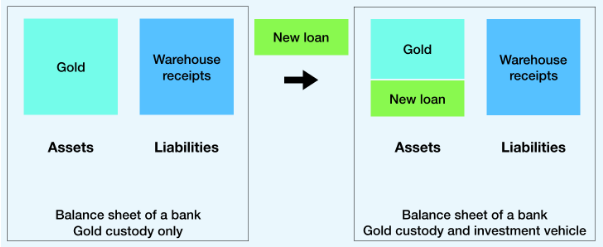

Lending during the gold standard

Larger quantities of gold were usually held at a bank that performed the above-mentioned function of gold custody. In addition to the business of custody, banks performed other activities such as lending. Banks thus acted as an investment vehicle. This is highly relevant for further analysis. Before that it must be noted that transparency is a top priority for investment firms: Investors need to know in which assets the firm is investing their money because investments are risky. But transparency is extremely limited in the case of banks until today. In my opinion, the separation of custody and investment is urgently needed to protect the saver and to assure more transparency for the investor.

During the original Gold Standard, the bank granted loans with its clients' money for which the bank paid interest in return. This corresponds to the transfer of money from the investor (client of the bank) through the investment vehicle (bank) to the investment (borrower) as known from venture capital or private equity funds. This new loan is then part of the bank's assets, as the bank is entitled to the loan amount plus interest. Part of the interest is paid by the bank to the actual lenders of the loan - the savers. This corresponds to the interest on the savings in our current system. The savings deposit is a liability from the bank's point of view, since the bank assures that the credit balance will be paid out when requested.

The process above describes the Gold Standard where no unbacked warehouse receipts are issued - I have called it the "original" Gold Standard. But as mentioned earlier, banks have often issued unbacked warehouse receipt during the Gold Standard. These unbacked warehouse receipts were mostly given out in the process of lending as illustrated in the figure below. Specifically, the borrower did not receive gold as credit, but unbacked warehouse receipts. Money was created "out of thin air" because these warehouse receipts were not backed by gold.

The fraud was not noticed as long as the bank's customers did not reclaim their gold in large amounts. In concrete terms, no more gold should be withdrawn than the custodian can serve with its gold. If more warehouse receipts are claimed than are covered by gold, the custodian can no longer service its liabilities to the savers and goes into insolvency. This usually happens during a bank run.

When the fraudulent behaviour of some banks became known, other banks refused to accept their warehouse receipts. Mistrust about whether these warehouse receipts were really covered with gold increased. The Federal Reserve System has "solved" this situation. Banks whose fraudulent behavior was exposed could then be "rescued" by a central bank. This means that the banks could then issue unbacked warehouse receipts with no limit. Here are the Federal Reserve's words about its function:

„By creating the Federal Reserve System, Congress intended to eliminate the severe financial crises that had periodically swept the nation, especially the sort of financial panic that occurred in 1907. During that episode, payments were disrupted throughout the country because many banks and clearinghouses refused to clear checks drawn on certain other banks, a practice that contributed to the failure of otherwise solvent banks. To address these problems, Congress gave the Federal Reserve System the authority to establish a nationwide check-clearing system.“ (Source: Federal Reserve System Publication, Purposes and Functions)

Money creation in the Fiat System

During the Gold Standard, the practice of issuing unbacked warehouse receipts was common. The central banking system provided a special incentive for this. From 1944-1973, during the so-called "Bretton Woods System", the US dollar was tied to gold. In this system, USD 35 corresponded to one ounce of gold. The system fell apart precisely because of unbacked notes: More US dollars were created than the Federal Reserve Bank of the USA had gold in custody for. These US dollars corresponded to the "unbacked warehouse receipts". But the textbooks say that the Bretton Woods system fell apart because of "trust issues" and "speculative attacks". Through this framing, the public was blamed for the collapse of the system, although this loss of confidence was justified because the US Federal Reserve had created more US dollars than were backed by gold.

Now the money is no longer bound to any underlying asset - the money has thus become so-called "Fiat money". The term "Fiat" comes from Latin and means "it is done". In this Fiat System, the practice of creating money from nothing is common banking practice. Below is a figure that explains the process of lending in the Fiat System. The process is analogous to the issuance of unbacked warehouse bills in the Gold Standard: the loan amount is simply added to both sides of the balance sheet. The money is not transferred, but instead is created out of thin air.

Banks can create money out of thin air not only in the process of lending, but also when they buy assets. The value of the asset is recorded on the asset side of the bank and the money is credited to the seller's account as illustrated in the figure below. This money is not transferred, but created from nothing - analogous to the process of lending. Corresponding articles on the processes can also be viewed directly on the websites of the German and English central banks.

Monetary systems in which money cannot be created out of thin air

The monopoly of creating money out of thin air contradicts the right to property. Savings are dwindling in value due to the money creation process described above. Assets such as real estate are becoming unaffordable for many people due to inflation as the purchasing power is reduced. The artificial central banking system leads to negative consequences for the economy such as boom and bust cycles, misallocation of resources and asset price bubbles. The question arises: How do we change this system? Here I would like to mention a quote from Buckminster Fuller:

"You never change things by fighting the existing reality. To change something, build a new model that makes the existing model obsolete." - Buckminster Fuller

What can a new system look like that eliminates the weaknesses of the old system? First and foremost, it must no longer be possible to create money out of thin air. This is the case with Bitcoin and Gold. As discussed in detail in this article, gold has fallen victim to the fraudulent behaviour of custodians: Custodians have issued more warehouse receipts than they held gold. This is still possible now. However, a functioning gold standard requires the trustworthy behaviour of custodians. But history has taught us that many custodians were not trustworthy, so we should learn from the past.

Bitcoins do not require a custodian to be sent over distance. Bitcoins can be sent over the decentralized network to the recipient over distance without a central authority. Bitcoin enables users to be financially sovereign themselves based on a technology that does not require a centralized authority. "Only" the self-sovereignty of the owner is required. This includes extensive study of this technology. A profound understanding of Bitcoin requires a critical examination of the most diverse areas of our lives: starting with economics, computer science, game theory, politics, law, and psychology.

")