An overview of what is happening in the crypto markets, summarised daily by Crypto Finance AG Senior Trader Patrick Heusser in the market commentary.

Global markets are under pressure again, which is dragging down the entire crypto space. So, let's focus on good old interest rates without the funky yield farming turbo boost.

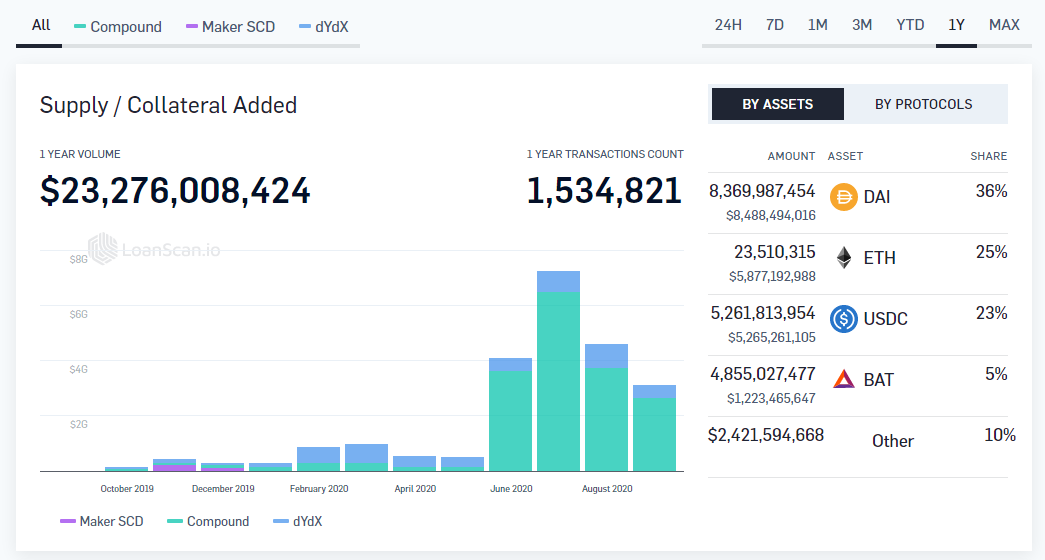

On loanscan.io, there is a very insightful overview of the decentralised borrowing and lending market landscape. It not only references crypto assets, but also stablecoins with their USD equivalence.

It definitely gives you a better feel for what kind of rates you can expect for a certain asset without taking additional risk (e.g. yield farming).

Let's start with the "Earn Yield" tab. These rates represent deposit rates for each asset.

They are displayed as APY (annual percentage yield), which takes the compounding effect into account. We discussed this in an previous DeFi commentary, where we compared APY with APR (annual percentage rate). For the ones who missed it, here is a link to Investopedia.

As you can see, the yields are all in the single digit percentage space (except for USDC on the Nuo platform, which is probably a missprint, since their borrowing rate is only at 2.19%). The business model is fairly simple. The platforms offer margin trading for various products (spot and derivatives), and their traders need to borrow the capital as a margin requirement. If you are long, you can deposit some of those wanted assets and earn yields. The risk is platform (counterparty) risk, which you can, in fact, break down into their margin call and liquidation procedure model. As long as these platforms have a solid understanding of how to handle the liquidation risks on their platform, your capital should be safe.

Borrowing rates are obviously higher, but also mostly in the single digit percentage space. It is also good to see that the spread between deposit and borrowing rates has tightened significantly. This points to the market being more efficient through better protocols and platform usability, but also on account of competition.

The last section is "Collateral". As you can see, it only represents roughly 35% of the DeFi TVL (if you believe that number represents the proper capital in use or at risk in the DeFi space). It is still a sizable share of this space. The reason why I look at these key figures is to get a sense of how stretched the system is. We will publish a Market Commentary on leverage in the DeFi space in the near future. The current situation looks pretty relaxed, and the number of liquidations that went through in early September were absorbed easily by the system.