A Federal Reserve research paper proposes regulation for the stablecoin ecosystem and calls for ways to address systemic risks. Their issuers should be regulated as banks and central banks should launch their own digital currencies (CBDCs).

A member of the Board of Governors of the Federal Reserve System as well as a Yale University professor propose oversight of the stablecoin ecosystem in a recently published paper, "Taming Wildcat Stablecoins". They call for addressing systemic risks, regulating stablecoin issuers as banks, and introducing central bank digital currencies (CBDCs). Furthermore, they conclude that privately issued stablecoins are not an effective medium of exchange.

Role of private money

According to the introduction of the paper, cryptocurrencies are currently trending again, although privately issued money is not a new phenomenon. The goal of private money, they argue, is to be accepted at face value. That didn't work during the Free Banking Era of the United States (1837-1862) - a period that most resembles today's world of stablecoins, the authors said. State-owned banks experienced panics during this time, and their private money made it difficult to settle transactions due to price fluctuations.

That system was curtailed by the National Bank Act of 1863. It created a single national currency backed by U.S. government bonds. Subsequent legislation abolished the paper currencies of government-run banks in favour of a single sovereign currency - the U.S. dollar.

Stablecoins like "Tether" and Facebook's "Diem" are the latest type of private money, according to the paper. Based on lessons from history, the authors argue that privately generated money is not an effective medium of exchange because it is not always accepted at face value, and is subject to further risks. The proposals presented address the systemic risks posed by stablecoins, including the regulation of stablecoin issuers as banks and the issuance of a central bank digital currency (CBDC).

Stablecoins as untamed "wildcats"

The research paper refers to privately issued currencies as "wildcats". In the future, they said, these could lead to governments having to step in with a bailout, because they are uninsured. They claim this could happen soon as stablecoin issuers become the money market funds of the 21st century. If left unchecked, stablecoins could evolve into an ecosystem reminiscent of the free banking era in the U.S. in the 19th century.

"If policymakers wait too long, stablecoin issuers will become the money market funds of the 21st century - thus "too big to fail" - and the government will have to step in with a bailout in the event of a financial crash. Moreover, preserving the government's monetary sovereignty is critical to monetary policy. Policymakers should learn from history, and not repeat the same mistakes." - Excerpt from the research paper, "Taming Wildcat Stablecoins."

The authors also talk specifically about the currently largest stablecoin Tether (USDT) and Facebook's Diem in the abstract. Thus, the focus is rather less on decentralized networks like Bitcoin (BTC). Numerous global bodies and high-level authorities in several countries have already commented on stablecoins in this context.

Increased regulation of the sector

Regulatory headwinds for stablecoins span multiple economies and agencies across government hierarchies. In one document, the Bank for International Settlements (BIS) proposes a hybrid and intermediary CBDC. Although stablecoins were not specifically mentioned in it, it is generally agreed that CBDCs would discourage the growth of stablecoins.

Authorities in the U.S. and EU have also discussed regulating stablecoins and cryptocurrencies. However, they spoke about it more in the context of money laundering and combating terrorist financing.

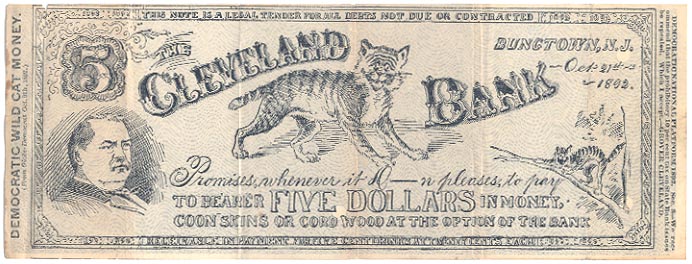

What are "wildcats" anyway?

The traditional view of wildcat banks describes them as distributing nearly worthless money backed by questionable collateral (such as mortgages and bonds). These actions ended when note circulation by state banks stopped after the passage of the National Bank Act of 1863. The face value typically decreased the farther away the place of redemption was from the issuer. A $5 bill from one state often did not have the same purchasing power as the $5 bill from another state.

According to some sources, the term originated with a Michigan bank that issued private paper currency with the image of a wildcat. After the bank failed, poorly backed bills became known as "wildcat money" and the banks that issued them became known as "wildcat banks". A common conception of the wildcat bank in Western novels and similar stories was that of a bank that displayed in its vault a barrel full of nails, grain, or flour with a thin layer of cash on top, fooling depositors into thinking it was a successful business. The Federal Reserve's comparison brings out well its aversion to privately issued currency.